Every Hong Kong limited company must undergo an annual audit. No exceptions. Whether you run a small trading firm or manage a multi-million dollar operation, the Companies Ordinance requires you to prepare audited financial statements each year. Getting this right protects your company from penalties and keeps your business compliant with Hong Kong law.

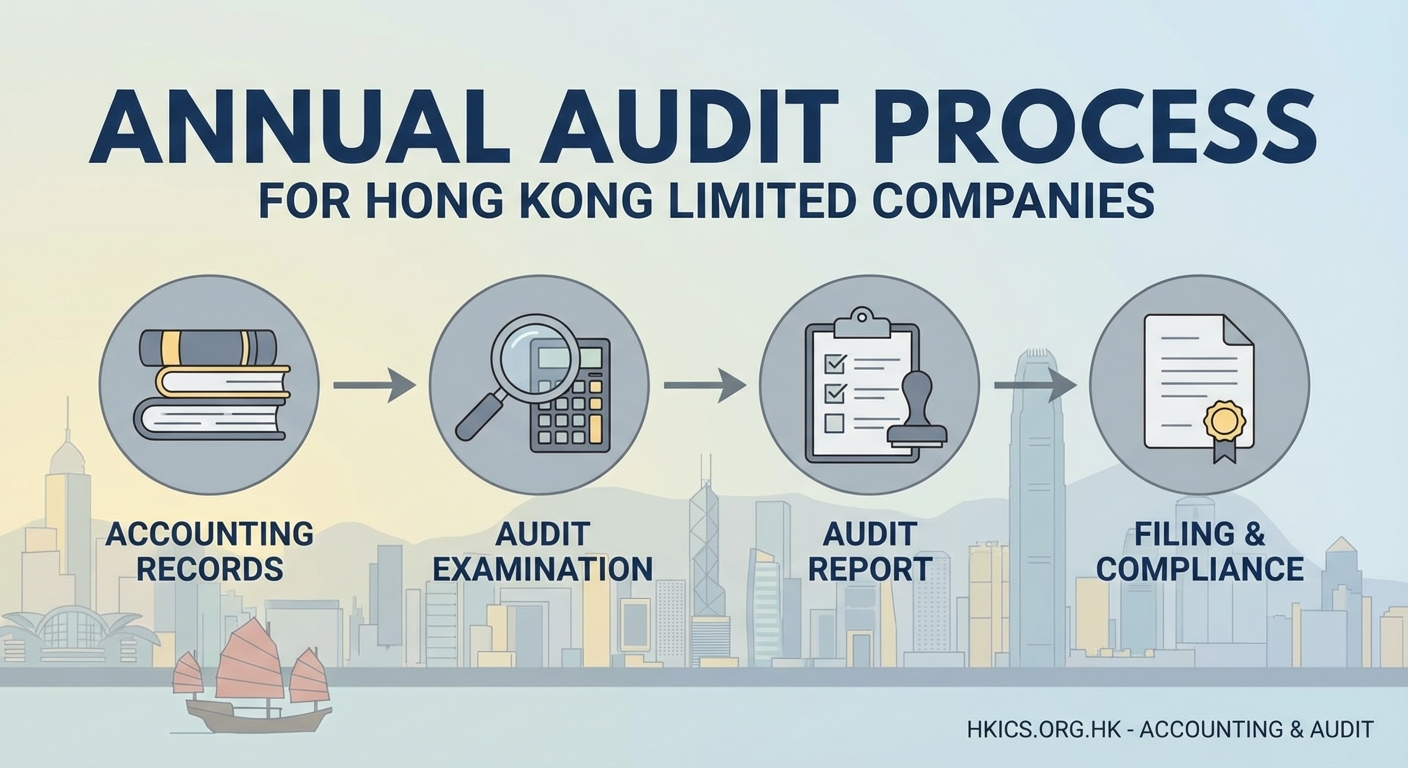

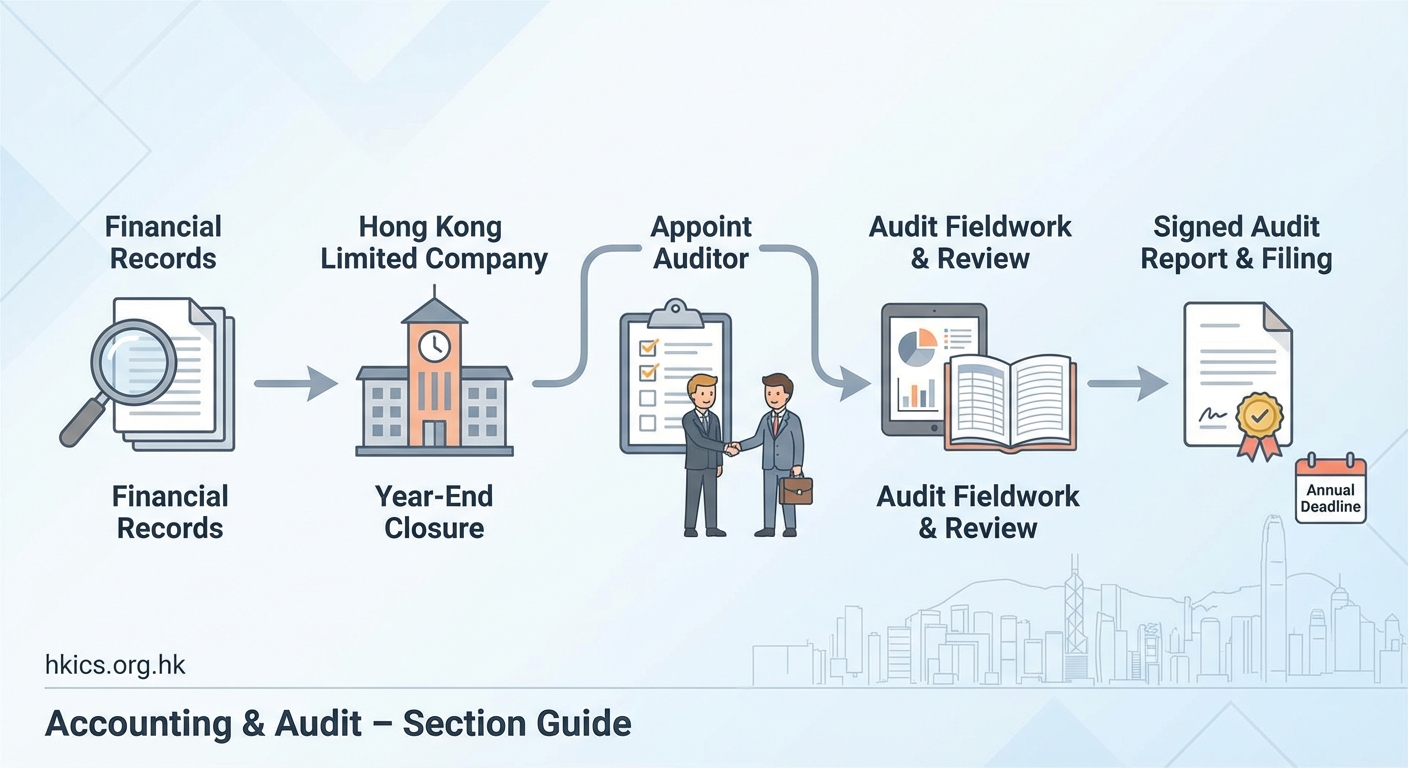

Hong Kong limited companies must complete an annual audit by a certified public accountant. The process involves preparing financial records, conducting the audit examination, issuing an audit report, and filing with the Inland Revenue Department and Companies Registry. Timelines depend on your financial year end, with specific deadlines for tax filing and annual returns. Proper preparation and choosing qualified auditors ensure smooth compliance.

Why Hong Kong companies need annual audits

Hong Kong’s regulatory framework mandates that every limited company, regardless of size or turnover, must have its accounts audited annually. This requirement stems from the Companies Ordinance and serves multiple purposes.

First, audited accounts provide transparency to shareholders and stakeholders. They verify that your financial statements present a true and fair view of your company’s financial position.

Second, the Inland Revenue Department uses audited accounts to assess your profits tax liability. Without proper audit reports, you cannot complete your tax filing.

Third, audited statements protect directors from potential liability issues. They demonstrate that the company maintains proper accounting records and follows recognized accounting standards.

The audit requirement applies from your first financial year. Even if your company generated zero revenue, you still need an audit report.

Who can perform your company audit

Not just anyone can audit Hong Kong company accounts. The law requires a certified public accountant who holds a practicing certificate issued by the Hong Kong Institute of Certified Public Accountants.

Your auditor must be independent. They cannot be a director, employee, or partner of your company. This independence ensures objectivity in examining your financial records.

Most companies engage audit firms or independent CPA practitioners. The size of your business often determines which type of auditor suits you best. Smaller companies might work with sole practitioners or small firms, while larger operations typically need firms with more resources.

When selecting an auditor, consider their experience with companies in your industry. An auditor familiar with trading companies might not be the best fit for a technology startup or property investment firm.

Preparing for your audit

Preparation makes the audit process smoother and faster. Your accounting records need to be complete and organized before the auditor begins their work.

Start by ensuring all transactions are properly recorded. This includes:

- Sales invoices and receipts

- Purchase invoices and payment records

- Bank statements for all company accounts

- Payroll records and MPF contributions

- Asset purchase documentation

- Loan agreements and related documents

Your bookkeeping should be up to date. Many companies maintain monthly or quarterly bookkeeping to avoid a year end rush.

Reconcile all accounts before the audit. Bank reconciliations, debtor and creditor confirmations, and inventory counts should be completed. These reconciliations help identify discrepancies early.

Gather supporting documents for significant transactions. Large purchases, major contracts, or unusual items will require additional documentation during the audit.

The audit process step by step

Understanding the audit workflow helps you know what to expect and when.

-

Planning meeting: Your auditor meets with you to understand your business operations, accounting systems, and any changes from the previous year. They assess risk areas and plan their audit approach.

-

Document submission: You provide the auditor with financial records, supporting documents, and account reconciliations. Most auditors now accept electronic documents, making this stage faster.

-

Fieldwork and testing: The auditor examines your records, tests transactions, and verifies balances. They might contact banks, customers, or suppliers to confirm information. This stage typically takes one to three weeks depending on company size and complexity.

-

Draft financial statements: Based on their examination, the auditor prepares draft financial statements. You review these for accuracy and completeness.

-

Audit adjustments: If the auditor identifies errors or necessary adjustments, they discuss these with you. You decide whether to adjust the accounts or disclose the items in notes.

-

Final review: After incorporating agreed adjustments, the auditor performs a final review to ensure everything is in order.

-

Audit report issuance: The auditor signs and issues the final audit report along with audited financial statements.

The entire process usually takes four to eight weeks from document submission to final report. Complex situations or incomplete records can extend this timeline.

Understanding your audit report

The audit report represents the auditor’s professional opinion on your financial statements. It comes in several types.

An unqualified opinion means the auditor found your financial statements present a true and fair view. This is the standard result for companies with proper records and no significant issues.

A qualified opinion indicates the auditor disagrees with certain aspects or could not obtain sufficient evidence for specific items. This raises red flags for tax authorities and stakeholders.

An adverse opinion states the financial statements are materially misstated. This is serious and rare.

A disclaimer of opinion means the auditor could not obtain enough evidence to form an opinion. This typically happens when records are severely inadequate.

Your audit report quality directly affects how tax authorities and business partners view your company. An unqualified opinion should always be your target. Anything less signals problems that need immediate attention.

Filing requirements and deadlines

After receiving your audit report, you must file it with government authorities within specific timeframes.

Profits tax return filing

The Inland Revenue Department issues profits tax returns annually. You must file your return within one month from the issue date, though extensions are commonly granted.

Your audited accounts must accompany the tax return. The tax computation shows how you calculated your assessable profits based on the audited figures.

Late filing without valid reasons results in penalties. The IRD can impose fines and, in extreme cases, prosecute directors.

Annual return filing

Separately, you must file an annual return with the Companies Registry. This return includes basic company information and must be filed within 42 days after your annual return date.

While the annual return itself does not require audited accounts, maintaining current audit reports ensures you can file accurately.

Common audit challenges and solutions

Many companies face similar issues during audits. Recognizing these helps you avoid delays.

| Challenge | Impact | Solution |

|---|---|---|

| Missing invoices or receipts | Cannot verify expenses, possible disallowance | Implement document retention system, use cloud storage |

| Incomplete bank reconciliations | Extended audit time, higher fees | Reconcile monthly, investigate differences immediately |

| Poor inventory records | Difficulty verifying cost of goods sold | Conduct regular stock takes, maintain perpetual inventory system |

| Related party transactions not documented | Tax authority scrutiny, transfer pricing issues | Document all related party dealings with proper agreements |

| Cash transactions without support | Potential income understatement concerns | Minimize cash dealings, use bank transfers, keep detailed cash books |

Addressing these issues proactively reduces audit time and costs while improving your compliance position.

Audit costs and what affects them

Audit fees vary widely based on several factors. Understanding these helps you budget appropriately.

Company size matters most. A dormant company might pay HKD 2,000 to 3,000 for audit services. An active trading company with moderate transactions typically pays HKD 5,000 to 15,000. Larger companies with complex operations can pay significantly more.

Transaction volume affects fees. More transactions mean more testing and longer audit time.

Record quality impacts costs directly. Well organized, complete records reduce audit hours. Messy or incomplete records increase fees as the auditor spends more time reconstructing information.

Business complexity adds cost. Multiple bank accounts, foreign transactions, intercompany dealings, or inventory all increase audit work.

Timing affects pricing too. Requesting audit services during peak season (March to May) when most companies file tax returns often means higher fees or longer wait times.

Maintaining audit readiness throughout the year

Smart companies do not wait until year end to think about their audit. Continuous preparation makes the process easier.

Keep your bookkeeping current. Monthly updates prevent year end backlogs and help you spot issues early.

File documents systematically as you go. Create folders for different document types and store them consistently.

Perform monthly bank reconciliations. This simple practice catches errors while they are fresh and easy to correct.

Review your accounts regularly. Monthly or quarterly reviews help you understand your financial position and identify unusual items.

Communicate with your auditor during the year. If you undertake unusual transactions or make significant changes, brief your auditor early. They can advise on proper treatment and documentation.

Special considerations for different company types

Different business models face unique audit considerations.

Trading companies need robust inventory systems. Your auditor will verify year end stock counts and test cost calculations. Maintain detailed records of goods purchased and sold.

Service companies focus more on revenue recognition and receivables. Proper documentation of service delivery and billing becomes critical.

Holding companies with investments need valuation support for their investment portfolios. Keep investment agreements, board minutes approving investments, and regular valuation updates.

Companies with related party transactions face extra scrutiny. Document all dealings with related companies at arm’s length terms. Transfer pricing documentation might be necessary.

Penalties for non-compliance

Failing to meet audit and filing obligations carries serious consequences.

The Companies Registry can prosecute companies and directors who fail to keep proper books or prepare audited accounts. Conviction can result in fines up to HKD 300,000.

Late tax filing incurs immediate penalties. The IRD charges HKD 1,200 for returns filed within three months of the deadline, increasing to HKD 3,000 for longer delays.

Persistent non-compliance can lead to company strike off. The Registrar can remove companies from the register if they fail to file required documents.

Directors can face personal liability. If the company cannot pay penalties, directors might be held personally responsible.

Beyond legal penalties, poor compliance damages your business reputation. Banks, suppliers, and potential partners view non-compliant companies as risky.

Choosing between audit firms and sole practitioners

Both audit firms and individual practitioners can serve your needs, but they offer different advantages.

Audit firms provide depth of resources. If your primary contact is unavailable, other team members can assist. They often have specialized industry knowledge across various sectors.

Sole practitioners typically offer more personalized service. You work directly with the qualified accountant throughout the process. Their fees are often lower for smaller companies.

Consider your company size and complexity. Simple operations might benefit from a sole practitioner’s personal touch and lower fees. More complex businesses might need the resources and expertise of a larger firm.

Check credentials regardless of firm size. Verify that the person signing your audit report holds a valid practicing certificate.

Digital tools and modern audit practices

Technology has transformed how audits are conducted. Understanding these changes helps you work more efficiently with your auditor.

Cloud accounting systems allow real-time access to your records. Your auditor can review transactions remotely, reducing the need for physical document exchange.

Electronic document management speeds up the audit. Instead of photocopying stacks of invoices, you can share files through secure portals.

Bank feeds automate transaction recording. Many accounting systems now connect directly to bank accounts, reducing manual data entry and errors.

Digital signatures enable faster report issuance. Once the audit is complete, reports can be signed and delivered electronically.

Despite these advances, the fundamental audit principles remain unchanged. Technology speeds the process but does not eliminate the need for proper records and professional judgment.

Making audit season stress-free

Annual audits do not need to be stressful events. With proper planning and organization, the process becomes routine.

Set up good systems from day one. Invest time in establishing proper bookkeeping procedures and document management. This upfront effort pays dividends every year.

Build a relationship with your auditor. Regular communication creates understanding and trust. Your auditor becomes a valuable advisor, not just a compliance requirement.

Plan ahead for deadlines. Know your financial year end and tax filing dates. Schedule your audit early to avoid peak season delays.

View the audit as a health check, not a burden. The process provides valuable insights into your financial position and highlights areas for improvement.

Keep learning about compliance requirements. Hong Kong regulations change periodically. Stay informed through professional updates and discussions with your auditor.

Your annual audit represents more than a legal obligation. It provides assurance to stakeholders, supports your tax compliance, and gives you confidence in your financial reporting. Approach it systematically, maintain good records throughout the year, and work with qualified professionals who understand your business. These practices transform audit season from a dreaded deadline into a manageable routine that strengthens your company’s financial foundation.